Personal Finance Basics

How to budget & track your spending

The next chunk of posts will circle back around to personal finance - a topic near and dear to my heart (as well as infuriating, since we don’t generally teach it in school). If you haven’t yet, I’d suggest reading this basic overview of personal finance first and then come back to this post. In this next series of posts I’m going to be expanding on each of the principles covered in the overview.

Step 1 is to spend less than you earn. Pretty straightforward, but if you’re most people, you likely don’t have a good idea of where your money’s going. The first step is to figure that out. You can’t make good decisions without good information. In Ye Olden Days you would need to track your spending by hand, on paper or maybe in a spreadsheet, but technology is here to save the day and make this all so, so much easier.

And that’s part of the point. This needs to be easy. Ain’t nobody got time to enter every single thing you buy in a spreadsheet by hand. If you build a complicated system, you’re less likely to stick with it, because it’s a lot of work…and if you don’t stick with it, it’s not going to help you. I much prefer simple, easy systems that don’t take much time or effort to keep going, so I can get on with the other important stuff in my life.

So the first thing to do is choose some expense tracking software. Mint used to be the default option, but Intuit apparently doesn’t like providing great software to people unless they can charge an arm and a leg for it, so they’re discontinuing it. Boo. There are lots of other options, but I’ve saved you the hassle of researching and have a few to recommend. They all do basically the same thing: they sync with your bank accounts and credit card accounts to import all of your transactions and stick them into categories, giving you an idea of where your money is going. Past that, it just depends on the level of sophistication you want. Here are my favorites:

Nerdwallet: the advantage is that it’s completely free. The disadvantage is that you can’t create your own custom expense categories, you’re stuck with what they provide (which is a fairly reasonable list).

Monarch Money: Nerdwallet on steroids. Costs a modest amount (you can use code MINT50 to get 50% off your first year, though), but the big advantage is you can create your own expense categories and create rules to automatically put expenses from specific merchants in the categories you define. If you want more granularity of your expense tracking than Nerdwallet can provide, or if you just have a more complex financial situation, Monarch is a solid option.

You Need a Budget (YNAB): been around for ages, well-known and well-liked in the personal finance space. Similar expense tracking functionality as Monarch, but really good for actually building and managing a budget over a given time period.

My suggestion is look at Nerdwallet first, because if it meets your needs, it’s free - cool, you’re done. If you find you’d like something fancier, try out one of the premium options.

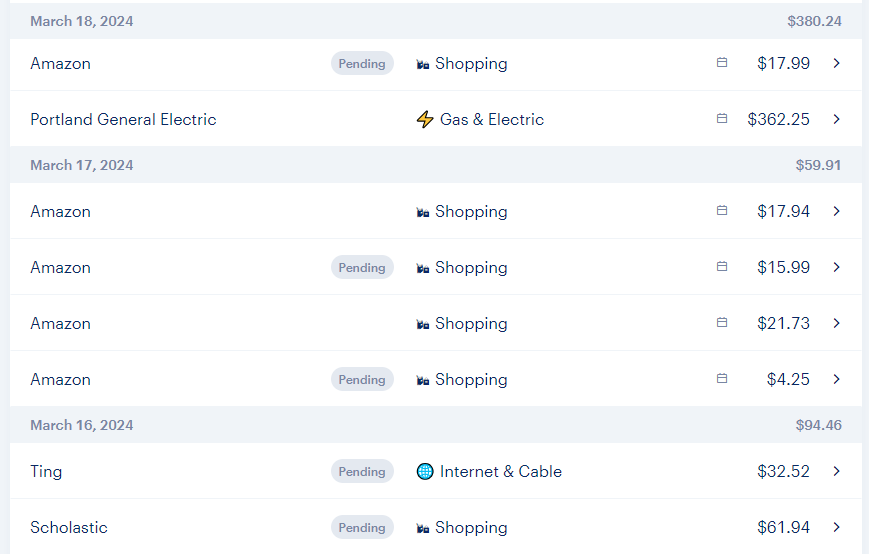

So, once you’ve set up your account, you then attach your other financial accounts by giving your expense tracker access to pull in transactions from your banks and credit cards (you can also have them track your investments/net worth as well, if you’d like). It’ll pull in all of your transactions, attempt to categorize them itself, and then you can go in and change the categories to make sure they’re what you want. In the beginning it will take a bit of effort, but as you go, you’ll create rules - you’ll teach it that you want anything from “Target” going into your “Grocery” category and anything from “Onlyfans” going into the “Professional Development” category, etc. It’s a bit of work at the start, but at this point I probably spend 5 minutes a month looking through my transaction record and making sure everything is in the right place. For example, here’s my recent transaction record in Monarch:

This is unedited (and I just recently transitioned from Mint to Monarch, so I don’t have my rules all set up yet). What I’ll do next is go click on “Internet and Cable” on the “Ting” line, because Ting is actually a phone provider, and change it to the “Phone” category. The “Scholastic” line is for my kiddo’s school book fair, so I’ll change that to my “Kid” category.

And if you want to see what it looks like for last month, here’s an example:

If you want, you can set up a budget in here as well. You can tell Monarch that you’d like to set a budget of $2,000 for food and dining, and then it would say something like “hey you were $202 over budget last month on food!” I don’t personally do that - but if you find yourself struggling with your finances (as in, not having enough money left at the end of the month), I think it’s an excellent idea. My recommendation here is don’t set up a budget right away - track your spending for a couple of months first. If you don’t know where you’re spending, any budget you set up will be completely arbitrary, but once you have an idea of your spending you can determine where you have room to reduce (or even where you have room to increase!).

At the end of the day, this setup serves two useful purposes. First, it tells you where your money is going. Did you realize how much you were spending on food per month, or on entertainment? Probably not if you don’t have a way to track and measure it. Second, if you’re having trouble making ends meet, it lets you see where you’re struggling. Is your food budget realistic? Are you spending too much going on and drinking at bars? If you ever find yourself puzzled at how you seem to be out of money at the end of the month, this is non-negotiable. You must do this in order to figure it out.

It’s easy for this to feel like a lot. Once you get past the initial set up phase, linking your accounts and getting the transactions in the right categories, it becomes incredibly easy and shouldn’t take you more than 5-10 minutes a month. Like I’ve been saying, it needs to be simple and easy, because that’s what makes it easy to stick with it over time. And it’s critical- you really can’t proceed with the rest of getting your finances in shape until you know where your money’s going.

If only we taught this in school.