Personal Finance Basics, Part 3

Don't get fucked by debt

In case the “part 3” didn’t make it obvious, this is part of a series. Start here if you haven’t read any of the personal finance stuff yet.

We live in a debt culture. Not all that long ago, debt was generally viewed as only being for mortgages, businesses, or emergencies. Now we take on debt for all kinds of things: college, cars, furniture…more and more businesses are adopting the “buy now, pay later” business model in partnership with fintech companies offering that as a service. And that doesn’t even consider credit cards, which we of course can use for just about everything.

You want some scary debt figures?

Total household debt in the U.S. is at an all-time high (which isn’t a surprise - it’s usually at an all-time high, it keeps going up every year). Total household debt reached $17.5 trillion at the end of 2023. For comparison, the U.S. GDP, as in the size of the entire economy, was a little under $28 trillion…so total household debt is getting close to equaling the entire economic output of the country for one year.

The average American consumer had $6,295 in credit card debt as of January 2024.

The average college graduate comes out of their 4-year program with $29,400 of debt.

Most new cars are bought on credit with an average car payment of $738/month as of early 2024.

If you want to unfuck your finances, you need to be extremely careful about debt. This is because debt can easily create a spiral - if you have some of what you think of as “manageable” debt (say, a car loan and some credit card debt you’re slowly chipping away at), it’s super easy to have some kind of emergency that forces you into MORE debt. A medical expense. The car breaks down. Something needs to be replaced that you weren’t expecting. Then it’s more debt. And it becomes harder and harder to climb out of. At some level it can even feel like “what’s the point, I’m so financially fucked it doesn’t even matter.” But you’re not. You’re almost certainly not so fucked it doesn’t matter, even if you have to declare bankruptcy, which can clear out most types of debt, and start over. You can make it out.

There’s a saying attributed to Albert Einstein that “compound interest is the 8th wonder of the world.” He never actually said that, but he was a pretty smart guy, so it sounds like something he would believe. Compound interest is what makes investing so great (which we’ll get into in the next article), but when you’re in debt, it works against you.

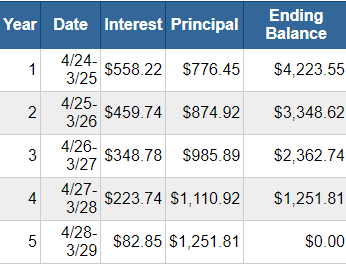

This is because paying off debt doesn’t work like you might think at first glance. Let’s say you borrow $5k at 12% interest. Your monthly payment is a little over $100. Not so terrible,right? But when you pay off debt, you’re paying more interest up front. At the start of the loan, a higher amount of the payment goes to interest and a lower amount goes to paying down the principal of the loan. As the loan progresses, a larger share of it goes to paying off the principal. This is called amortization. Let’s take our $5k loan at 12% interest, and let’s say it was a 5-year loan. Here’s how that loan amortizes:

In the first year, roughly 42% of your total payments go to interest. In the last year, it’s just 6% going to interest.

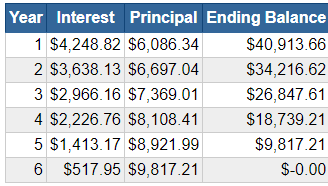

But if the monthly payment doesn’t change, why does it matter? Well, we often take on debt to buy stuff. And that stuff can be replaced, or sold. Think of a car. The average price of a new car this year is about $47,000. Let’s say you buy one and take out a 6 year, $47,000 loan at 9.6% interest (roughly average for folks with middling credit scores). Here’s what that amortization table looks like:

Pretty similar percentages to the first example. Lots of interest up front, with most of the principal pay-down happening later in the loan. Now let’s say after 3-4 years you decide you want another new car. Or, let’s say you get into a car accident and the car is totaled - the insurance will give you the full value of the car, but that’s all they pay, they don’t care how much you still owe on it (i.e. you can have a car accident that isn’t your fault, have your car wrecked, and insurance may not give you enough money to pay off the loan on the now-dead vehicle). This is because cars lose money - new cars generally lose 15-20% of their value in the first year, and then another 15%ish per year for the next few years. This is called depreciation (whereas if something gains value over time, that’s appreciation).

So remember our $47k car? Well, after 3 years it’s maybe worth something like $27k. And after 3 years, you owe…just about $27k on it. You may think something like “I’ve paid down half the loan on this thing, maybe I can sell it for something new and not have to borrow as much.” But as it turns out, if you sell your car, you have $0 to show for it. You’ve made $700-something monthly payments for 3 years and paid over $10,000 in interest. Yikes.

The point here is to be extremely careful taking out loans to buy depreciating assets. You’re paying more over time for something that becomes worth less over time. See how that’s bad?

Look, there are times when we need to take on debt. For most of us, we need to borrow money to buy a house (but in that case, houses usually appreciate in value over time). Many of us need to borrow money for college (more on in a future article, though). Many of us may even need to borrow money to buy a car because we need a vehicle and have no other option. That’s ok. The point isn’t to berate you for doing what you need to do, the point is to help get you to a point where you aren’t forced into decisions like that. Maybe right now you need to borrow money to buy a car, but once you get your shit together, you won’t be in that situation in the future.

If you’re faced with needing to buy something that you can’t afford (as in, you would need to borrow money to pay for it, but it’s something you cannot go without), strongly consider buying as little as you possibly can. Don’t buy a brand-new car on credit. Hell, most people shouldn’t be buying brand-new cars anyway, they’re a terrible value…but definitely not on credit! Buy the cheapest car you can reasonably live with, and then at some point in the future when you can actually afford to buy a nicer car without debt, you can choose to do that (as long as it doesn’t break your budget and aligns with your spending priorities and values!).

General rule: the only thing that is almost always “fine” to buy with debt is a house. College may or may not be fine, and that’s a more complex topic that we’ll dig into in a future article. A car may be necessary, but you don’t really want to buy it with debt. Anything else? Emergencies only. Don’t buy furniture, or fancy dinners, or vacations, or whatever else unless you can actually pay for it. Oh, and remember those unexpected expenses I mentioned earlier? That’s what the emergency fund you built as part of the last step is for! That’s its whole purpose: it lets you cover an unexpected expense without going into debt for it, and then you can replenish it afterwards (just make sure you actually replenish it).

It’s a very simple principle: debt is almost always bad, and if you stay away from it, your financial life will be not just more plentiful but also a whole lot less stressful. When you’re tracking where your money goes, living within your means, and have an emergency fund for any unexpected stuff, you can avoid being caught in the death debt spiral.